Q3 2024 Office Market Insights: Stability, Regional Growth, and Emerging Trends

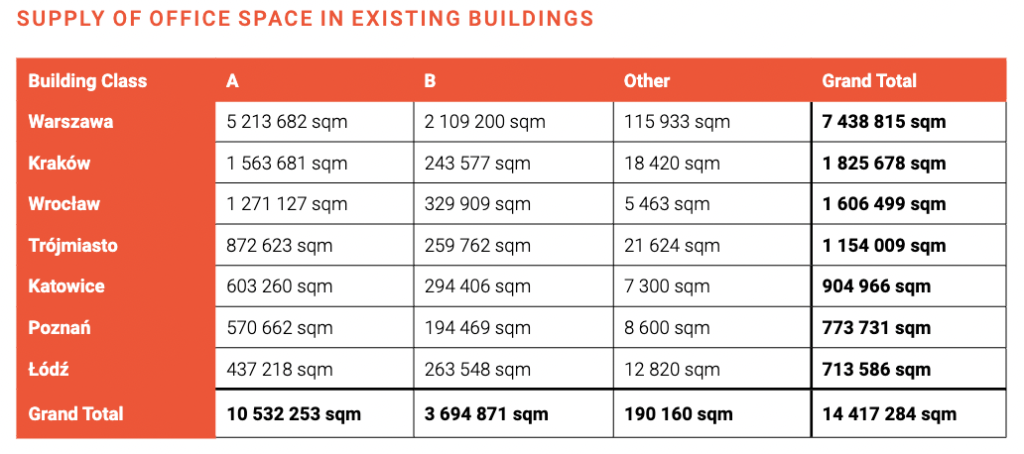

In the third quarter of 2024, the total supply of office space reached 14.4 million sqm, with Class A buildings accounting for the largest share at 7 million sqm. Warsaw, holding over 50% of the market, remains a key hub, yet new developments in cities like Wrocław, Kraków, and Tricity highlight regional growth. The highest amount of new space was delivered in Wrocław (26,600 sqm), while Gdynia saw the completion of two buildings totaling 14,500 sqm. The total area under construction reached 435,500 sqm – with nearly half of this located in the capital. In other cities, these figures are considerably lower; for example, Kraków has 54,400 sqm and Poznań has 51,300 sqm under construction.

VACANCY RATE AND RENTAL TRENDS

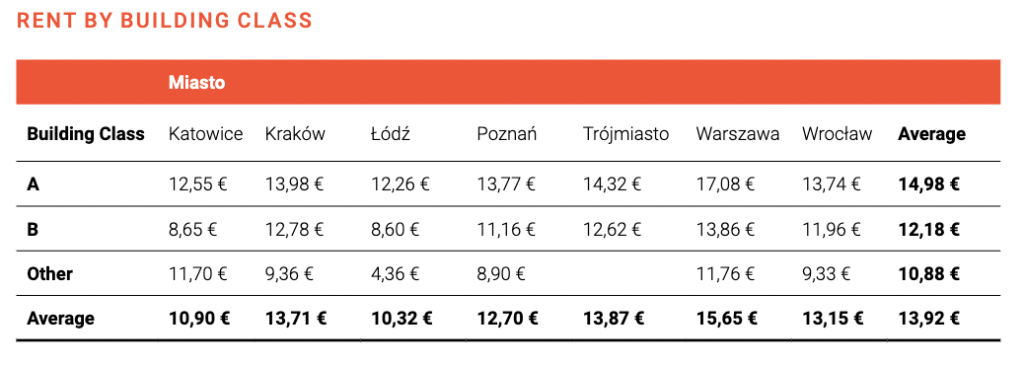

The average vacancy rate remains stable at 12.86%, with the highest rates in Łódź (21.4%) and Katowice (16.7%), and the lowest in Warsaw (10.2%) and Tricity (10.6%). The average asking rent increased, reaching 13.84 EUR/sqm, especially for prestigious Class A buildings, where rates approached 15 EUR/sqm. In Class B buildings, however, the rate declined to 12.18 EUR/sqm. Service charges remained stable – in Class B buildings, the amount was unchanged (19.68 PLN), while in Class A buildings, it increased slightly by 0.03 PLN/sqm, reaching 23.22 PLN/sqm.

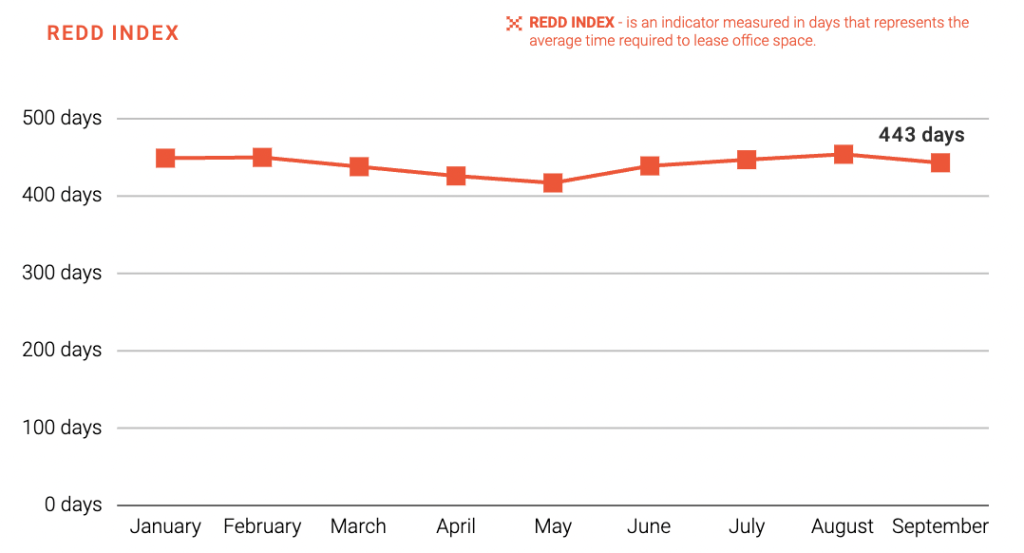

It’s also worth noting the average time needed to lease office space, calculated with REDD’s proprietary REDD Index. After a spike to 454 days in August, the index decreased to 443 days by the end of September.

Q3 2024 OFFICE MARKET FROM THE EXPERTS’ PERSPECTIVE

Marek Ciunowicz, COREES POLAND: Although the market is challenging and faces numerous obstacles, the situation in Q3 of this year was stable, with some signs of revival. A notable trend is the gradual return of employees to the office, along with optimizing the balance between on-site and remote work in favor of the former. Lease renegotiations were frequent, driven by the expiration of pre-pandemic leases. Rental costs continued to rise. Adapting to the evolving needs of employees, who now prioritize not only convenient access to public transport and office amenities but also well-being factors, remains challenging. Hence, the availability of spaces designed to improve mental and physical well-being has become essential. Employees are also increasingly attentive to ‘green’ aspects, indicating a growing awareness and desire to act together for the planet’s benefit.

Piotr Szmilewski, CEO of WOLF MARSZAŁKOWSKA: We see a growing trend of corporate clients considering flexible office spaces as an alternative to traditional offices. Initially, we focused on individual clients and small businesses looking to rent individual desks or small rooms. Now, there’s a significant increase in interest from global brands seeking spaces ready for immediate use with 50, 100, or even 250 workstations. This is partly due to the limited supply on the traditional office market and the lengthy setup time, which can take 9-12 months. In our spaces, the entire process can be completed within a few weeks. Amidst low office supply, subleasing may be an option for companies, but while this product offers faster availability, it lacks flexibility.

Jakub Denus, Leasing Manager, ADVENTUM GROUP: The office market in Poland has undergone and will continue to undergo dynamic changes compared to previously known ‘standards’. Minimum five-year lease terms and ‘turnkey’ fit-outs financed by the landlord – in the absence of rental rate increases – will likely become a thing of the past. The ever-growing expectations of tenants for more flexible lease agreements mean that investment funds are increasingly open to exploring various collaboration models with serviced office and coworking operators. They treat such services as excellent amenities and complements to their projects. Some investment funds are even investing in their own flex office concepts recognizing the potential to attract and retain both new and existing tenants within their properties. Changes in the commercialization strategies of existing office buildings are becoming more frequent than in the previous years.

We invite you to read the full REDD report. Download it via the form below.

Report

We Will Send the Report to Your E-mail Address

Download Report

All Done!

Report has been sent to provided e-mail address.

Please provide your business e-mail address.

Report has been sent to provided e-mail address.

All-in-one platform for CRE professionals

Single source for lease rates, available spaces and transaction history. Analytics and reporting capabilities. Landlord contact information. Complete oversight and real-time data updates.

Explore the platform