The Warehouse Market in the Face of Change: A 2023 Summary and 2024 Forecast

Economic and political factors, rising energy prices, and increasing inflation are just some of the reasons for the dynamic changes that affected the Polish warehouse market in 2023. The last several months have posed a significant challenge to the industry. Trends that clearly dominated this period were the dynamic increase in rental costs and the rising vacancy rate.

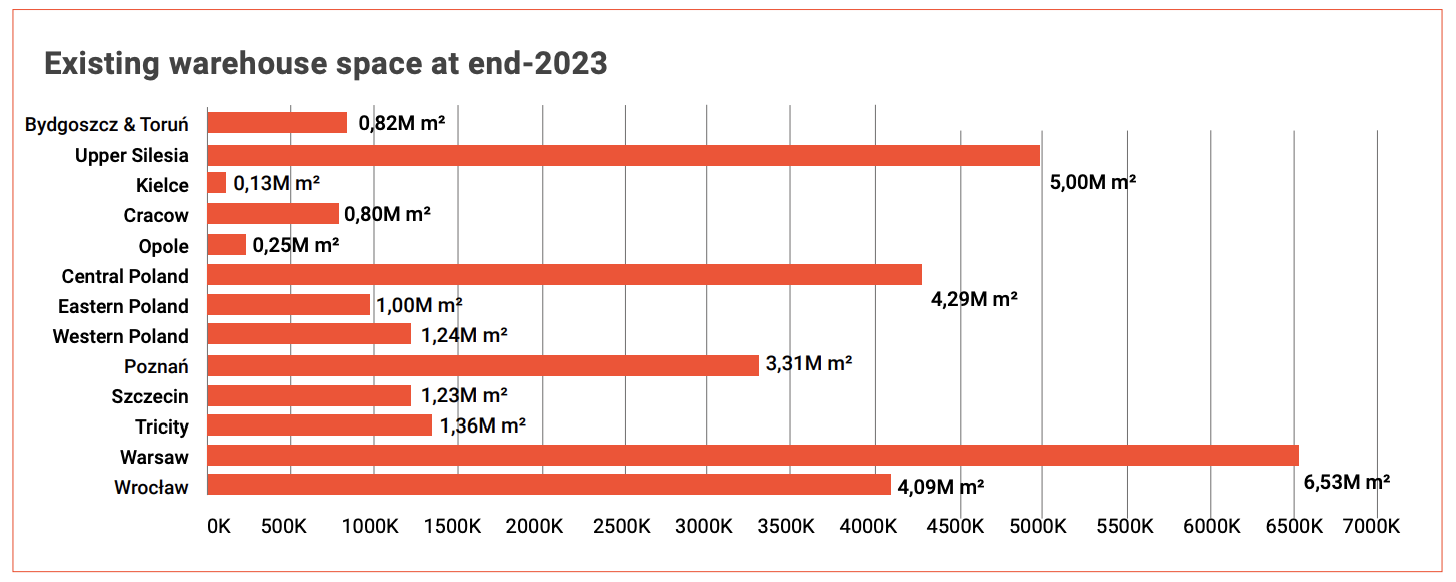

30 million square meters – that was the total supply on the warehouse market in Poland last year. For several years, the largest resources have been concentrated in the country’s five main markets. The supply in Warsaw, Upper Silesia, Central Poland, Wroclaw, and Poznan amounted to over 23 million square meters – which is as much as 3/4 of the entire market.

Smaller regions such as the Tri-City area, Western Poland, Szczecin, and Eastern Poland, meanwhile, exceeded the number of 1 million square meters of space.

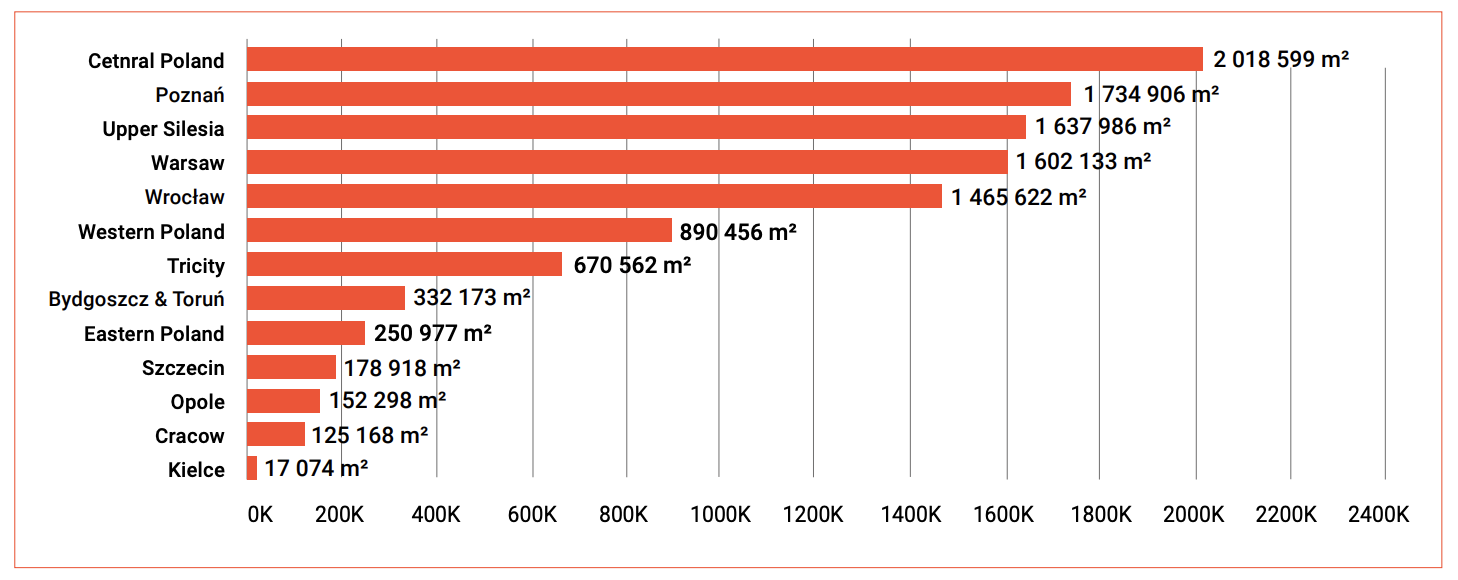

In 2023, 3.4 million square meters of new space hit the market. The most investments were made in the Wroclaw region, Warsaw, and Western Poland. Under construction were 2.5 million square meters – the vast majority in key markets such as Warsaw, Wroclaw, Central Poland, and Upper Silesia.

By the end of the year, the market offered tenants over 2.23 million square meters of immediately available space. Regions with the largest amount of vacant square meters were Warsaw, Upper Silesia, Central Poland, Poznan, Wroclaw, and Western Poland. In other markets, the size of immediately available space did not exceed 100,000 square meters.

The Polish warehouse market is continuously growing – currently, the construction of nearly 11 million square meters of warehouse space in 380 buildings is planned. The largest potential for the expansion of the warehouse supply base is currently in Central Poland, Poznan, Upper Silesia, Warsaw, and Wroclaw.

An important signal for the industry is the rising vacancy rate, which at the end of 2023 stood at 7.5%. The most such spaces were found in Western Poland (19.4%), and the least in the Tri-City area (1.5%).

What awaits the warehouse market in 2024?

In 2024, we forecast further, albeit slightly slower, rent increases, which will require flexibility and strategy adaptation by companies to new market conditions. Moreover, we observe an increasing business commitment to sustainability issues (ESG) – says Krzysztof Foks, Head of Research at REDD Group.

Piotr Flugel, Managing Director Poland, CTP: The primary trend driving the development of the industrial logistics sector in Poland is nearshoring, which began in previous years. However, the implementation of such investments takes time, leading to relatively low implementation dynamics despite widespread discussion.

Paweł Sapek, Senior Vice President and Regional Head for Central and Eastern Europe, Prologis: Considering that the vacancy rate has indeed been trending upward since the onset of 2022, reaching a notably high level nearing 8 percent in the third quarter of 2023, it’s reasonable to anticipate that positive developments may not yield immediate, significant impacts. Consequently, developers face the challenge of retaining existing customers and attracting new ones to fill the increasing number of vacant warehouses. In this context, ESG measures and investments in modern, cost-efficient warehouse parks assume greater significance.

Michał Ptaszyński, Country Manager, Logicor Poland: However, customers are still cautious, and their decision-making process takes longer. That’s not only because of high inflation but also because of the geopolitical situation affecting the global supply chain. Hence the phenomenon called nearshoring, where production and assembly lines are increasingly moving to the nearest sales markets. Due to its geographical location and relatively low barriers to market entry, Poland can benefit from this trend.

Tomasz Puch, Co-Founder, Managing Partner, BTV: For quite some time, there has been talk about Build-to-Own (BTO) warehouses. However, over the past three years, this trend has gained momentum, with even companies that previously leased space increasingly considering this option. All signs suggest that the BTO trend will continue to rise, propelled by nearshoring initiatives spurred by the streamlining of post-pandemic supply chains, ESG demands, and the prevailing global geopolitical landscape.

Dorota Mogielnicka, Owner, Greensite Consulting: In recent years, there has been a significant shift in the logistics sector towards sustainability, evident in the elevation of construction standards for industrial and warehouse buildings and the focus on environmentally-friendly operation. While the term ESG traditionally pertains to institutions and businesses, environmental stewardship extends to the realization of logistics facilities.

Explore the in-depth REDD report focusing on office space dynamics throughout 2023 and 2024, aptly titled “Stabilization at Last?” Access the full report by completing the form provided below.

Report

We Will Send the Report to Your E-mail Address

Download Report

All Done!

Report has been sent to provided e-mail address.

Please provide your business e-mail address.

Report has been sent to provided e-mail address.

All-in-one platform for CRE professionals

Single source for lease rates, available spaces and transaction history. Analytics and reporting capabilities. Landlord contact information. Complete oversight and real-time data updates.

Explore the platform